Midsummer Grain Update

More action on the demand side than normal for Summer

It’s been a busy month for grain markets. Weather has remained very positive for yields, and more and more commentators are starting to wonder what a 1994 event would look like in 2025 (185? 187?) and this has understandably weighed on prices. At the same time, the One Big Beautiful Bill Act and continuing trade uncertainty are undermining soybean exports and casting a pall over prices.

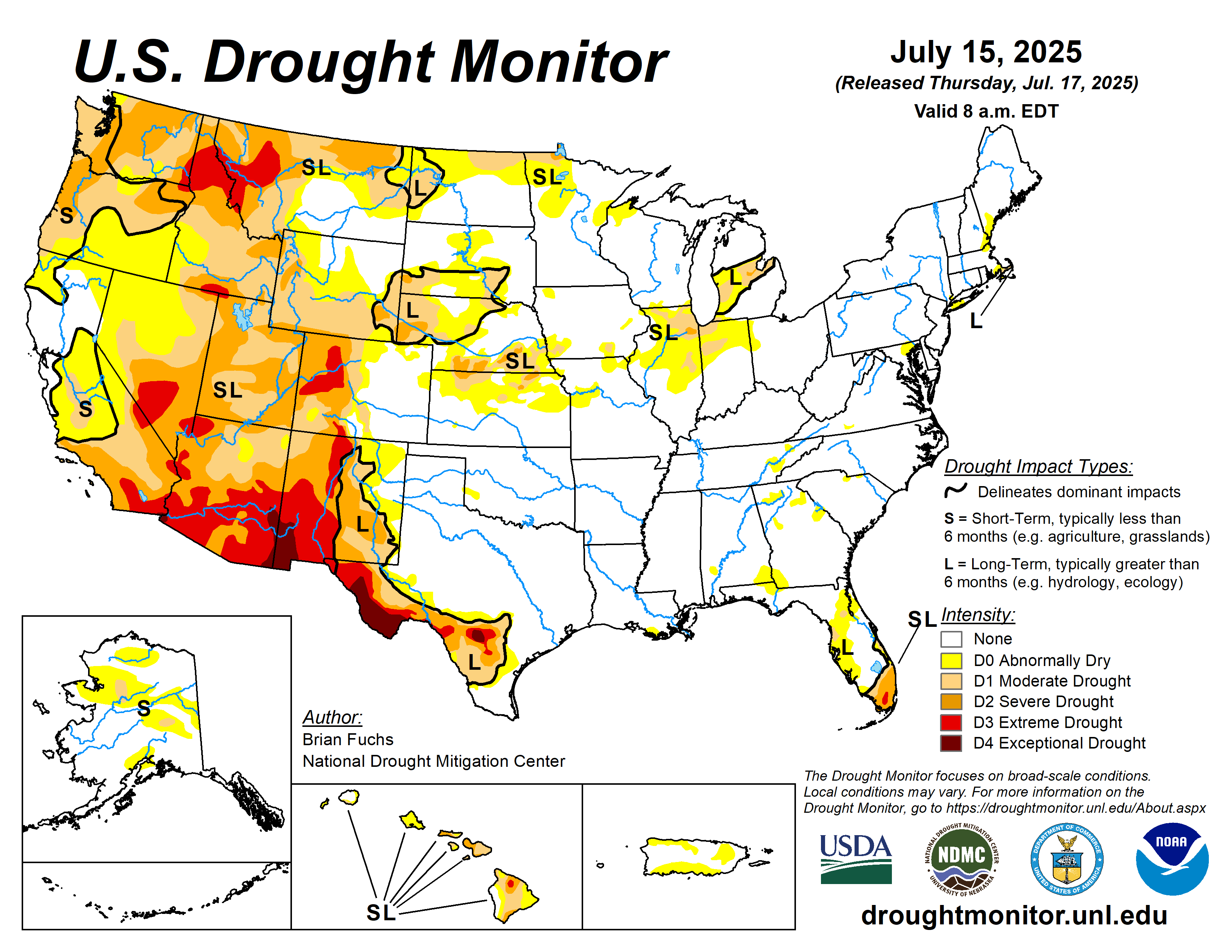

Starting with the weather; I’m not sure the last time that I’ve seen such a friendly drought monitor in mid-July. From a midwestern perspective, it’s not just affecting row crops, either. I was home in Southwest Missouri for the 4th, and there was a lot of baling going on. I don’t ever recall seeing that density of bales in the fields in July. If the past decade’s cattle herd numbers have been held back by some combination of balance sheet, profitability, or pasture and forage availability, that won’t be the case in 2025. I expect that the beef herd is already growing, and this will hopefully provide some additional grain demand in the coming years. In the July WASDE, feed use (across all species) is forecast to rise about 120m bushels when combining corn, wheat, sorghum, barley and oats. I believe that this is too low; and expect to see another 25-40m bushels of feed demand added as we go through the marketing year.

Wheat exports remain a surprise this year. While market conditions (lower prices, weaker USD, and lower EU exports) and USDA reports have continued to project higher exports, the market continues to run ahead of even these projections. The July report projects 850m bushels of exports in the 25/26 marketing year, but historically, we are on pace for 950m bushels. It is still relatively early in the year to go wild with upwards revisions, but I expect to see the August exports to increase by 25m bushels if we see this pace continue.

Soybean export pace is worrying. Between the large South American crop, and the uncertainty surrounding contracted pricing six months hence, the weakness in prices and the USD haven’t been able to result in higher exports. In better news for the soy complex, the OBBBA does place significant new restrictions on 45z tax credit eligibility. Starting in 2026, only feedstocks from USMCA countries will be eligible for 45z credits. This final language resulted in a huge boost in soybean oil prices as domestic tallow and UCO supplies are simply not large enough to meet the already existing demand.